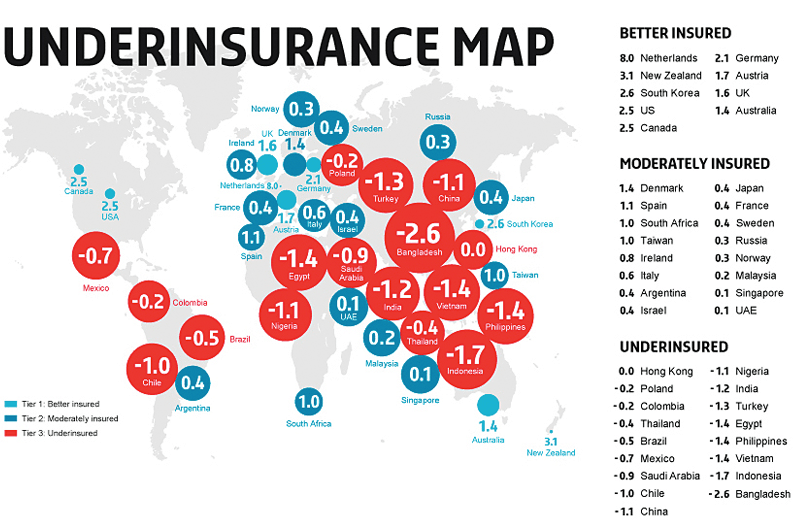

Are you underinsured?

Underinsurance is a critical issue: post-loss it may mean the difference between survival and failure. If you insure for the wrong amount you may not receive the full value of your loss if you have a claim. This is the case even with a partial loss — if the overall sum insured is inadequate, insurers will apply an “average”. This means they will reduce the claim settlement figure in proportion to the level of under-reported insurance value.

To put the problem in context, if you insured your building for GBP4 million — but it would cost GBP5 million to rebuild it — then suffering property damage totaling GBP500,000 would only result in your insurer paying you GBP400,000 (less any policy excess). You would have to find the remainder of the money (GBP100,000 and any policy excess) yourself. Because you are 20% underinsured the claims settlement is also reduced by 20%.

SOME COMMON CALCULATION ERRORS

• Calculating the sum insured using the original cost, net book value, or acquisition price of the property, rather than the cost of reinstatement.

• Ignoring recent changes like additional buildings and/or machinery.

• Using the wrong rebuilding indices to correct the value of your assets. For example, inflation factors affecting construction costs are sector and geography-specific. General inflation is an incorrect basis but is commonly used.

• Using indices over a long period.

• Failing to include items such as the costs of car parks, access roads, perimeter walls, and landscaping.

• Neglecting the allowance made for specialist circumstances, such as: – Listed status. – Known asbestos. – Special constructions. – Rare materials used. – Lead times for the replacement of specialist machinery. – Shortage of replacement machinery.

• Overlooking allowances made for currency fluctuations in respect of specialist equipment that must be sourced overseas.

• Failing to update sums insured to reflect changes in the business, such as a new acquisition, the development of a new product, or general growth during the year.

• Underestimating the limit needed for extension clauses, such as professional fees and debris removal. Standard provisions of 15% of the sum insured often prove insufficient.

I would advise that you have a professional valuation of buildings and contents carried out every three to five years. Professional valuers should take account of building materials, increases in labour costs, professional fees, debris removal, and plant hire costs. They will normally advise on the additional provisions necessary to reflect price increases during the rebuild period. Once a professional valuation has been carried out, buildings, plant and equipment sums insured can be adjusted annually for inflation by applying one of several indices used by valuers and contractors in the construction industry.

These indices rely on the base figure to which they are applied being accurate and up-to-date. Also, average building costs in most indices cannot accurately reflect variations in different types of structures or detailed geographical variations. Therefore, you may need to use your knowledge of the local labour market and specialist conditions as part of the calculation process.

There are also various cover options available in respect of material damage insurance, which can help to protect you against future inflation costs and the impact on your sums insured. In some instances, we have been able to negotiate policies without an average clause, where clients have had a professional valuation undertaken.

Naturally if you would like to discuss this or any other insurance policy, please don’t hesitate to contact one of our team on 0800 083 4933